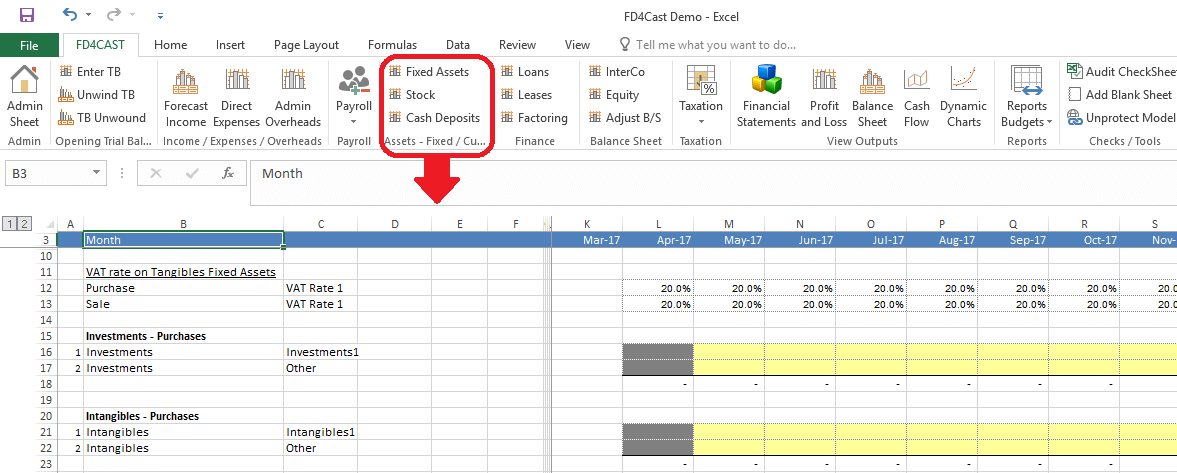

Both Current and Fixed Assets can be accessed from the Assets’ section on FD4CAST ribbon:

At the top of the Fixed Assets section you can find the VAT rates that apply to purchases and sales of assets. VAT rates can be managed from Taxation > VAT Assumptions on the ribbon. For more details on how to manage the tax rates, please, review Section 6.1 VAT & Currency Assumptions.

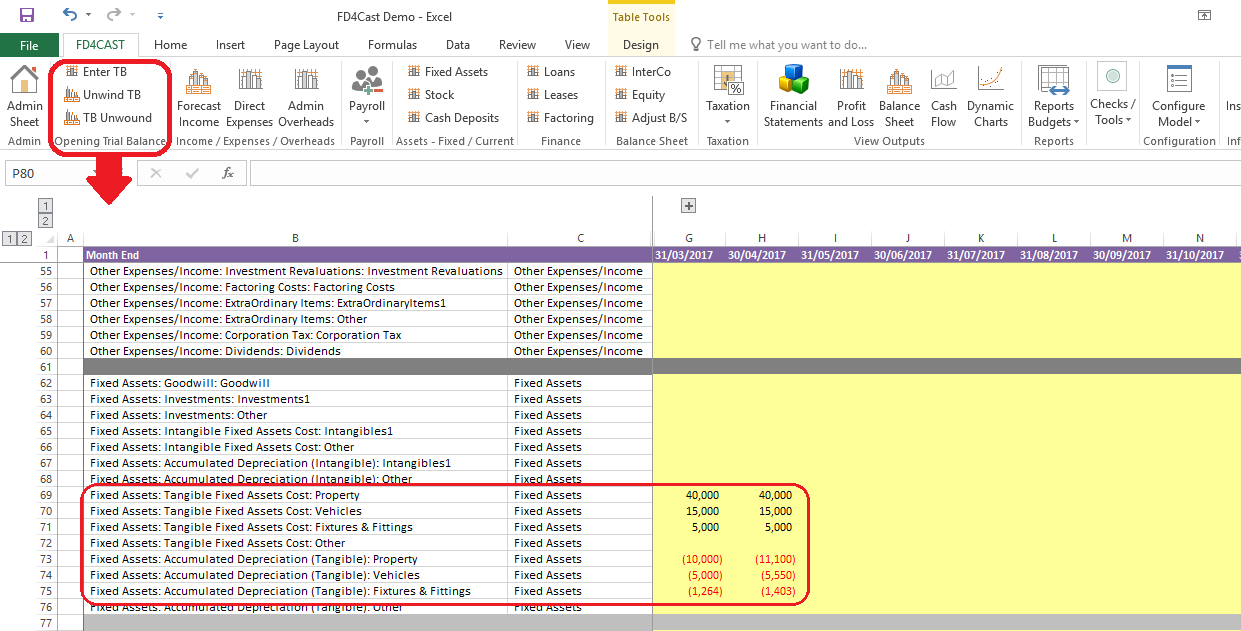

Fixed Assets are grouped into three categories – Investments, Intangible and Tangible Assets.

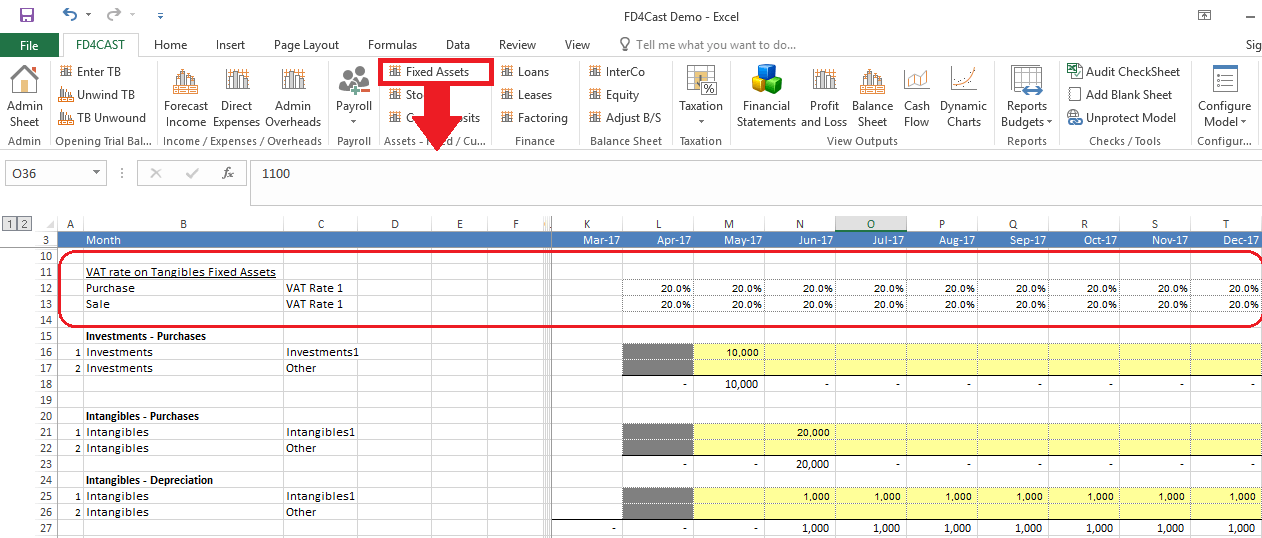

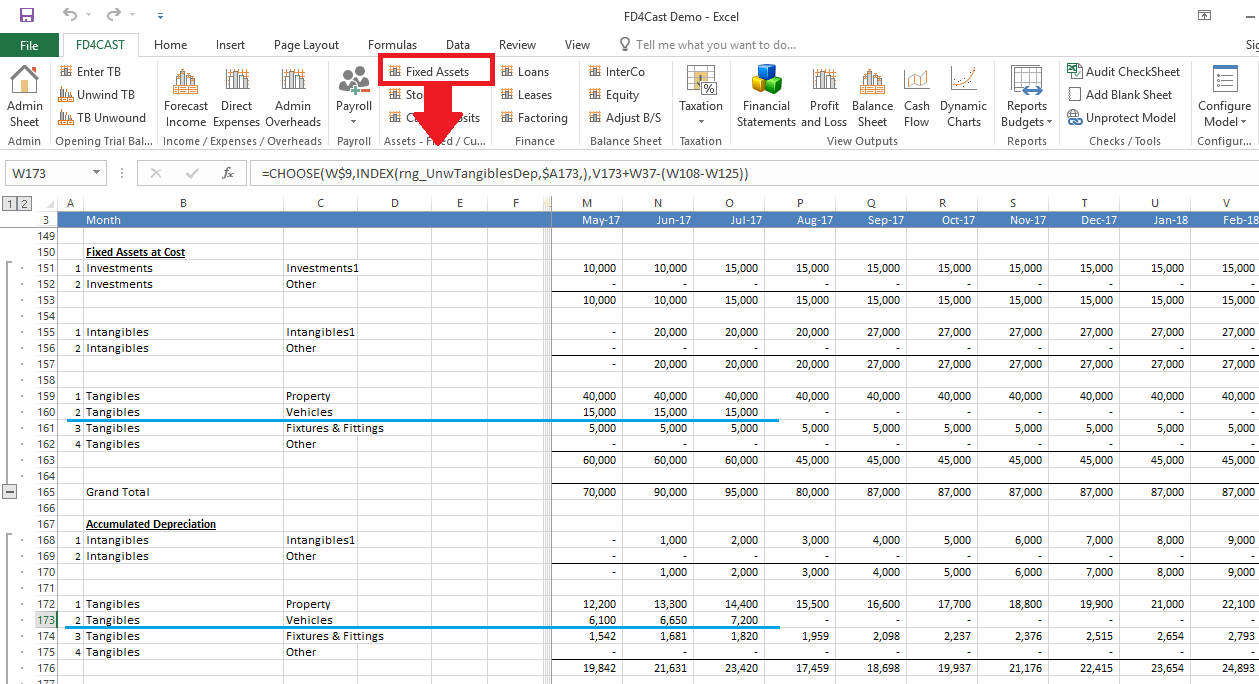

All fixed assets, with the exception of investments, are subject to depreciation. Keep in mind that both purchases and depreciation figures should be entered as positive numbers in yellow cells. Assets in this section are reported net of VAT as shown on the Balance Sheet.

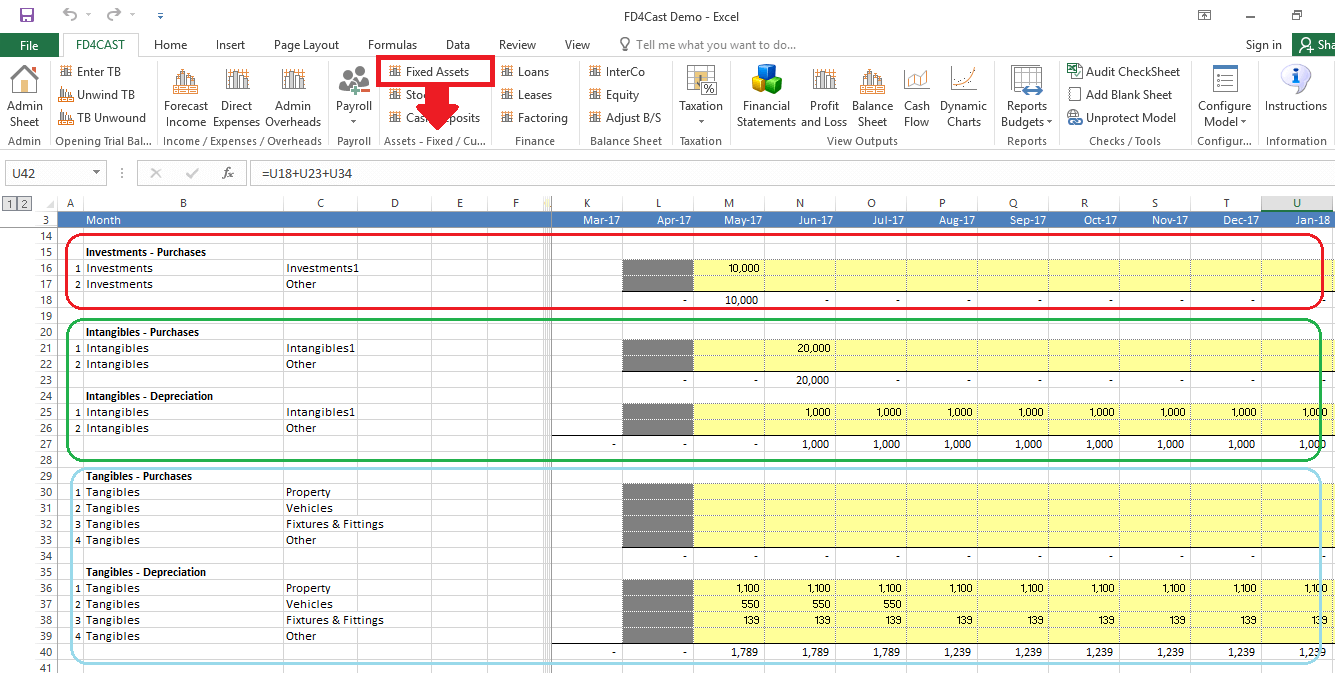

Depreciation for assets brought forward from before the forecasting period should also be reported in this section. E.g. figures shown under ‘Tangibles – Depreciation’ section above relate to fixed asset balances from previous periods as shown below.

Instructions on how to manage initial balances can be reviewed in Section 2: Inputs Balance.

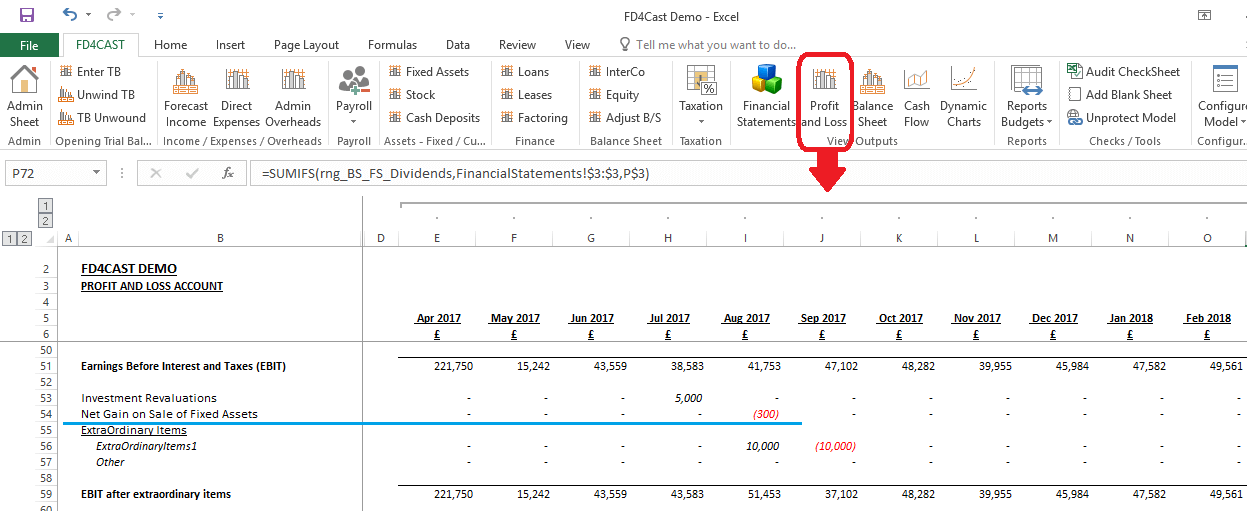

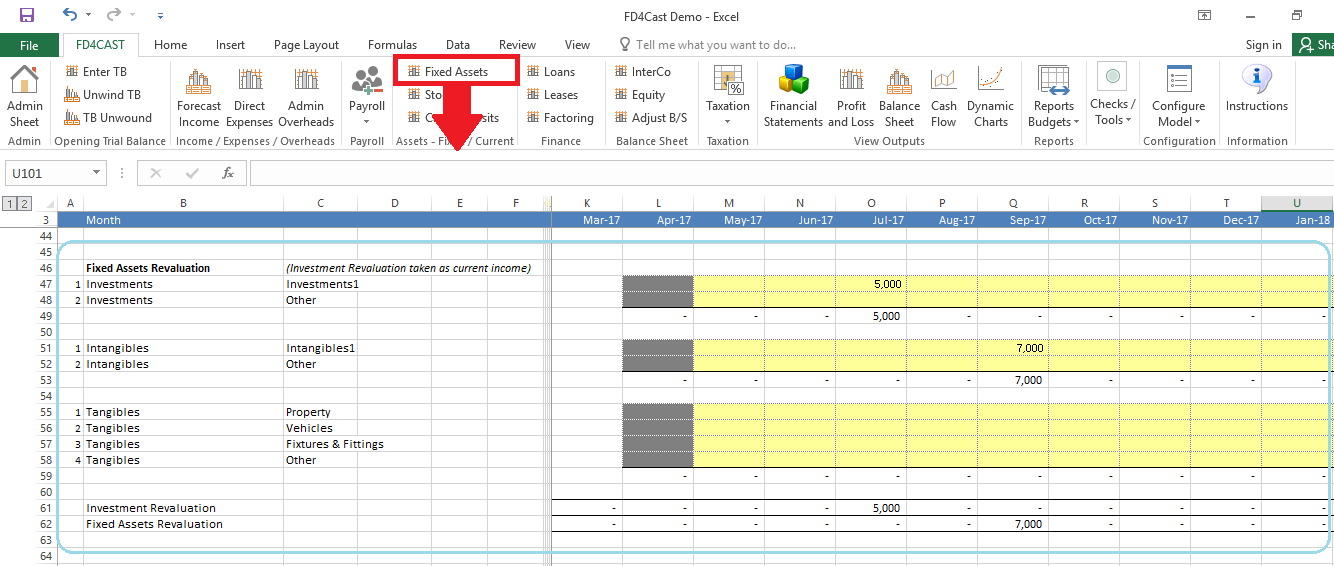

Model allows users to perform revaluation of fixed assets. Both upward and downward revaluations are reported in section below:

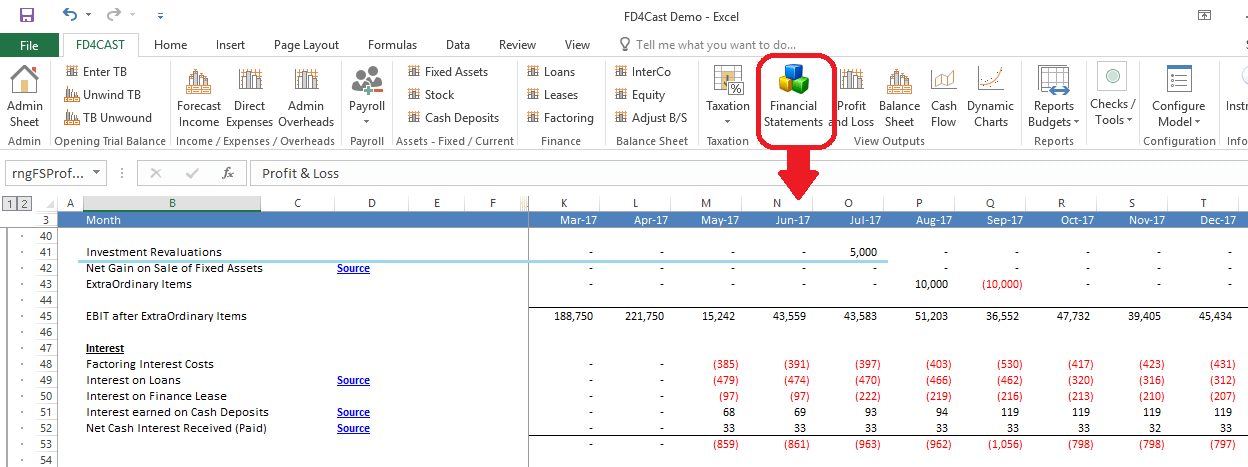

Investment Revaluation gains/losses (+/-) are reported in P&L under the line item, ‘Investment Revaluations’:

Revaluation gains/losses (+/-) from tangible and intangible fixed assets are not reported in P&L. They are reflected directly on the Balance Sheet under ‘Revaluation Reserves’. Reversals of previous revaluations will offset this Equity item directly, bypassing the P&L.

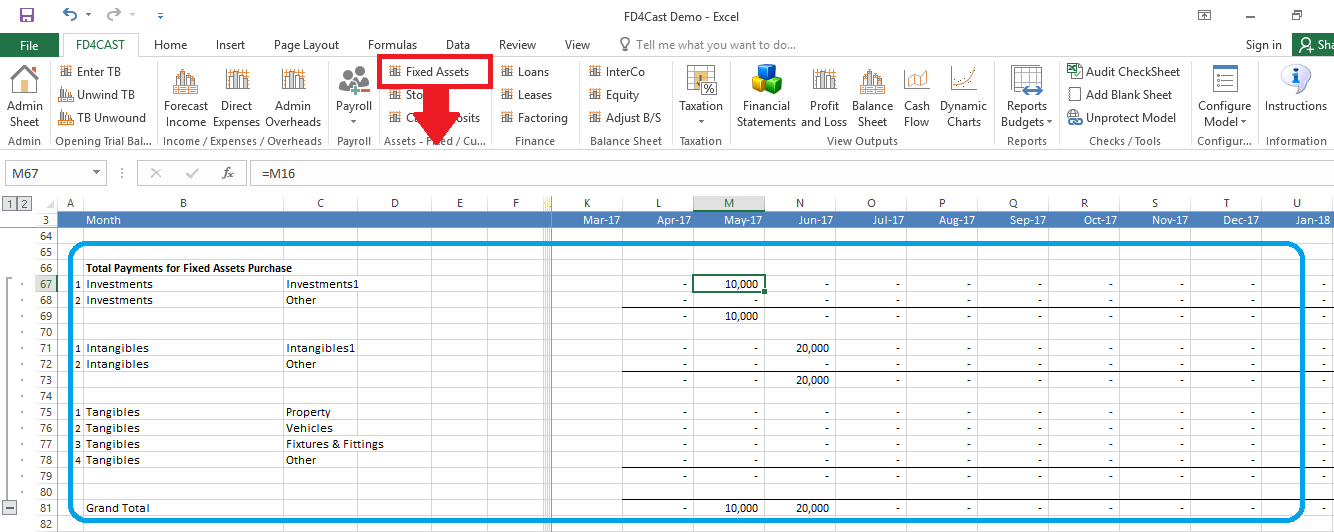

In our model it is assumed that payments for Fixed Assets take place in the month of acquisition. In the example below, payments for £10,000 worth of investments and £20,000 worth of intangibles take place in May-17 and Jun-17, in the same period as they were purchased. In order to reschedule payments, user will need to unprotect the model and manually apply the new payments schedule. Please, review Section 8.6 – Unprotect Model to review the instructions.

Keep in mind, that applicable VAT rate is automatically added to the cost of tangible fixed assets in the above section.

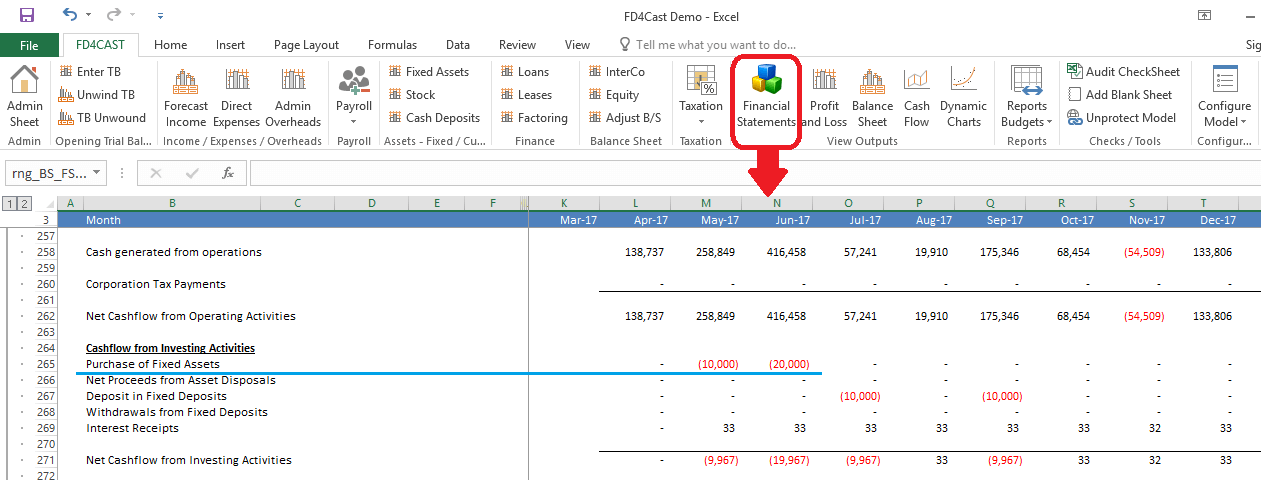

Above transactions are reflected in the Statement of Cash Flows (both direct and indirect), under the item, ‘Purchase of Fixed Assets.’

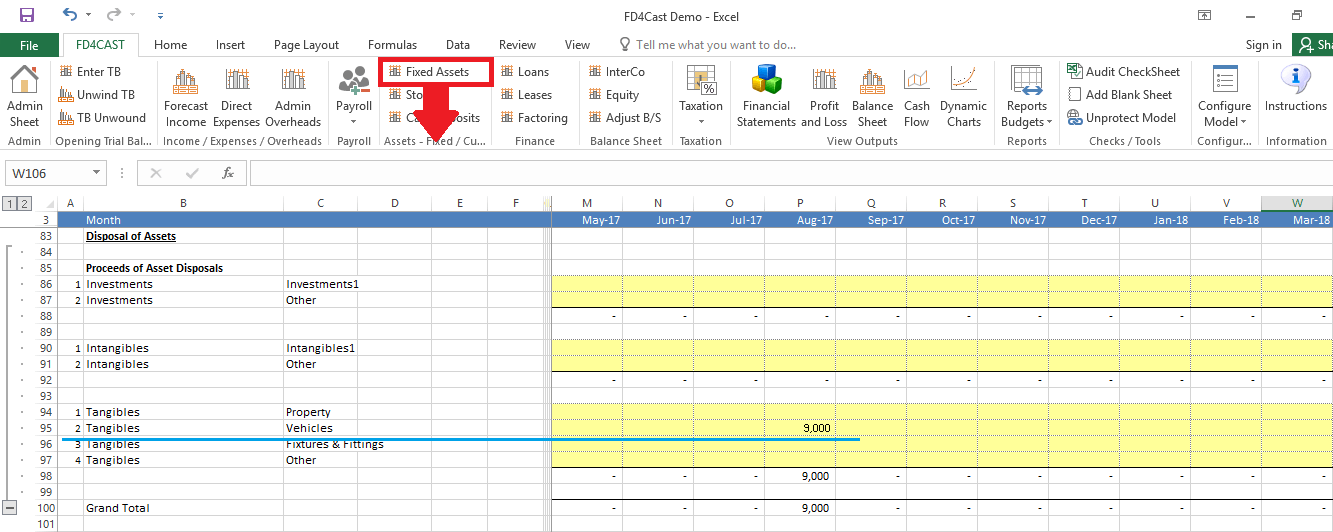

In order to correctly reflect the sale of fixed assets, we need to have the following three pieces of information:

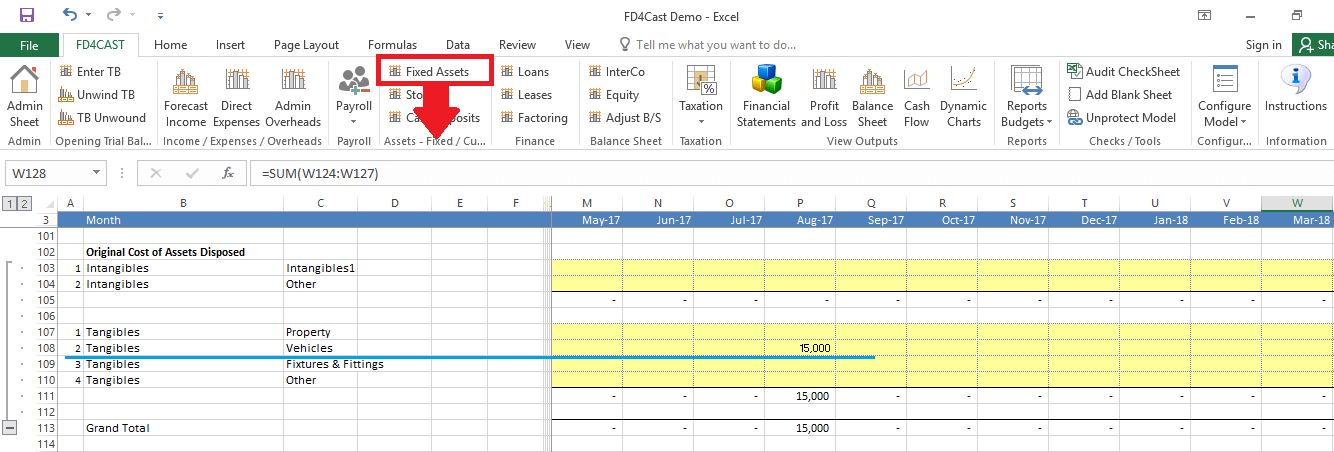

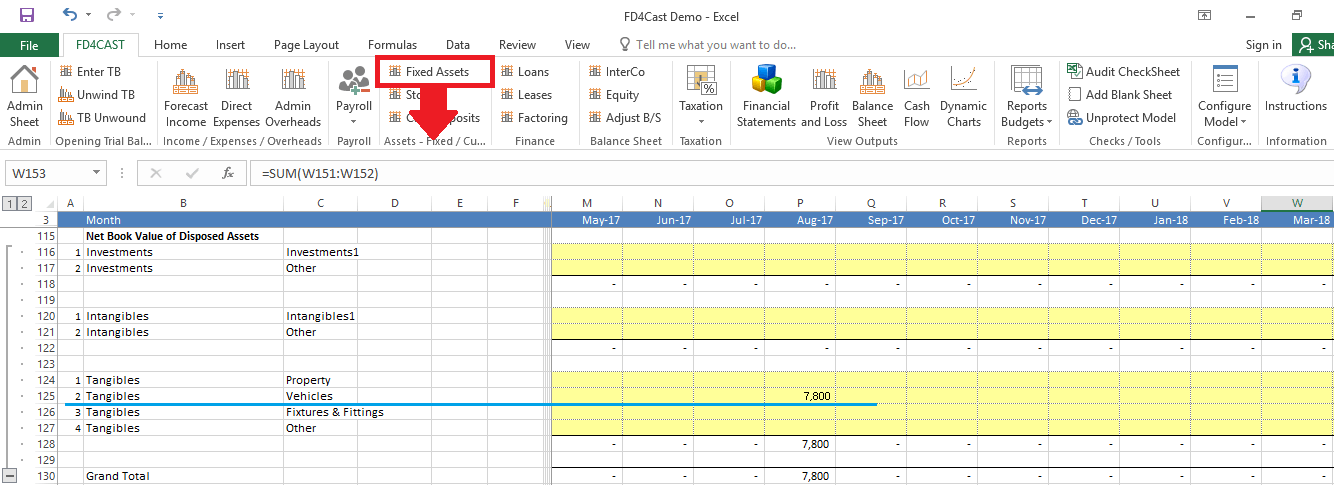

As an example, let’s assume that in the beginning of Aug-17, we plan to sell Vehicles with an original cost of £15,000 and the accumulated depreciation of £7,200. Net book value is £7,800 – the difference between the above two figures. The sales price is £9,000 including VAT.

We enter the above information in corresponding sections under Fixed Assets:

Proceed of Asset Disposals:

Original Cost of Assets Disposed:

Net Book Value of Disposed Assets:

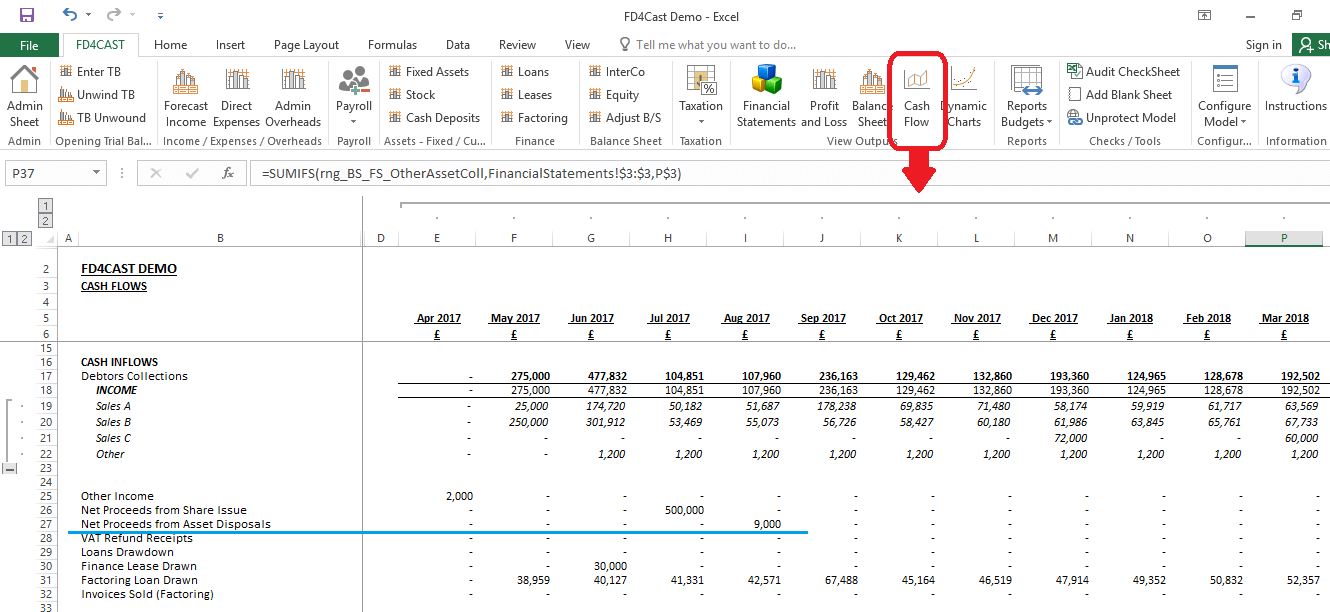

Disposal of fixed assets has an impact on all three financial statements. In the Statement of Cash Flows we can see inflow of £9,000 – proceeds from the sale of Vehicles including VAT:

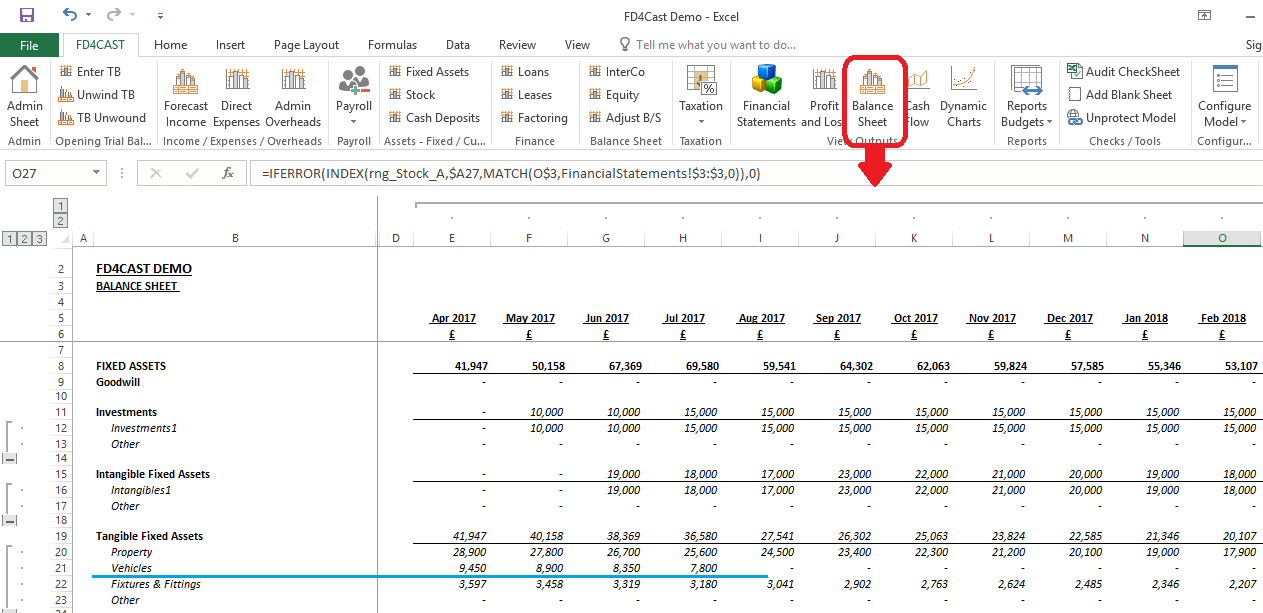

Vehicles, after they have been sold, do not appear on the Balance Sheet starting from Aug-17:

The Statement of Profit & Loss shows net loss on sale of fixed assets in the amount of £300 – difference between Proceed from disposals net of VAT (£7,500) and Net book value of Vehicles (£7,800).