All equity transactions of the company are managed through the Equity section from the Balance Sheet group on the ribbon.

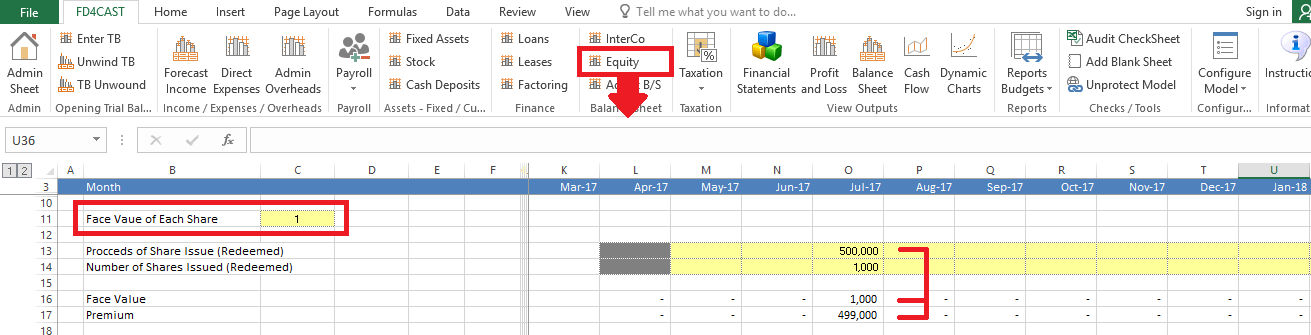

At the very top of the Equity section user can reflect issuing of new shares, their face value and total proceeds from the transaction.

In the example above, face value per share issued is £1.00. Total number of shares is 1,000 as entered in yellow cells next to the heading, ‘Number of Shares Issued (Redeemed)’. (In case of redeeming old shares, their quantity and amount should be entered as negative figures.)

If total proceeds from share issuance is £500,000, £1,000 (face value per share x number of shares) will be reported under Share Capital on the Balance Sheet. The difference between the total proceeds and the face value – £499,000, will be reported as Share Premium.

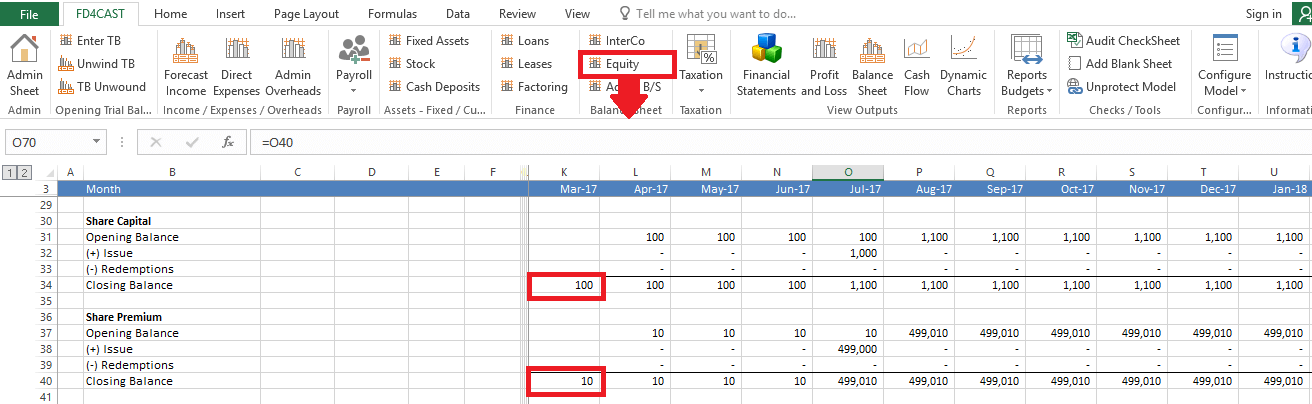

In the same Equity Section we can see the reconciliation of opening and closing balances for both Share Capital and Share premium accounts.

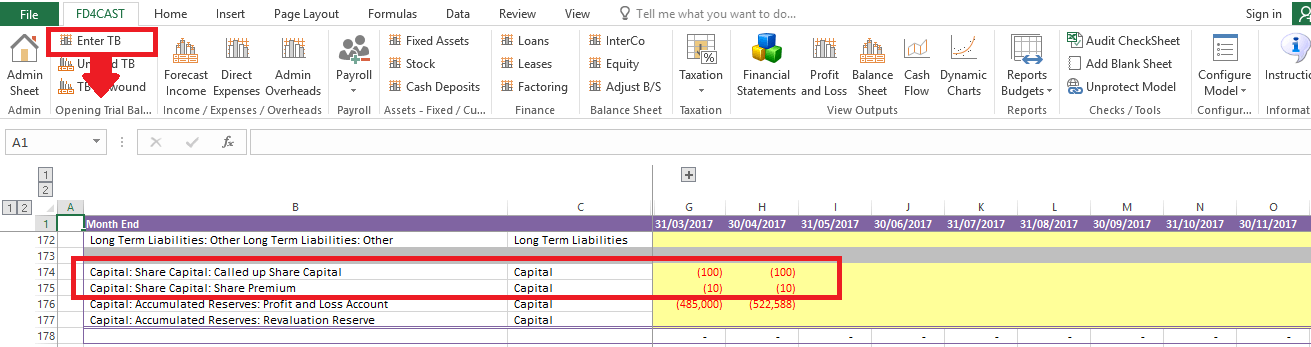

In our example, opening balances of Share Capital and Share premium are £100 and £10, respectively. These amounts come from Opening Trial Balance input section. For detailed instructions on how to bring forward opening balances, please, review Section 2: Inputs: Balance.

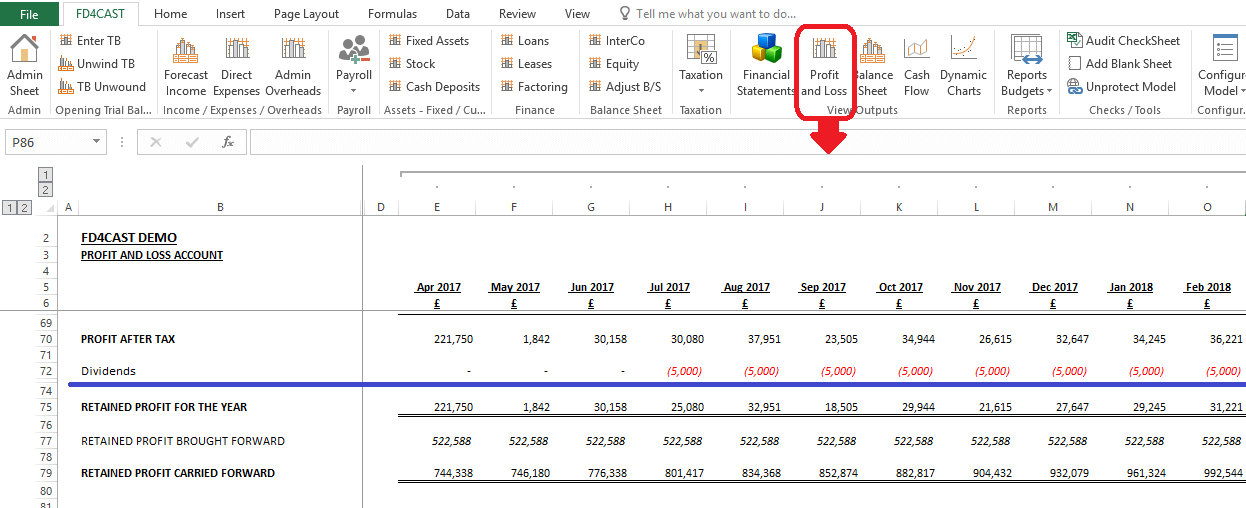

Declaration and payment of dividends are managed from the Dividends section.

Declared dividends are entered as positive figures in yellow cells above. It is assumed that dividend payouts take place in the same period as they are declared. In order to reschedule payments, user needs to unprotect workbook as explained in Section 8.6 Unprotect Model.

Declared dividends are reported in P&L below the Profit After Tax line item:

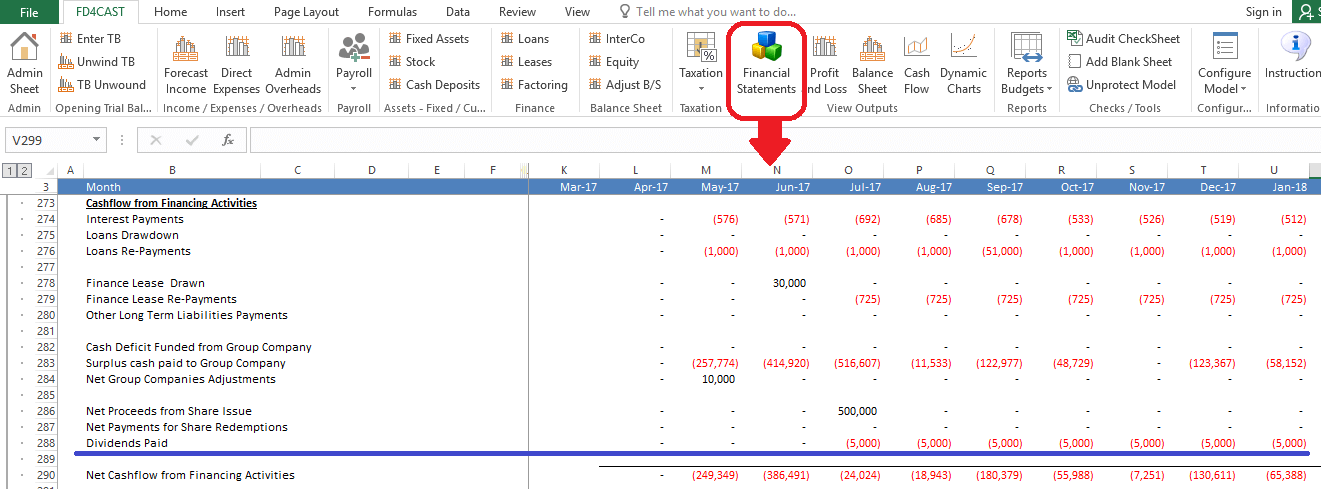

Payment of dividends are shown on the Statement of Cash Flows under Financing Activities:

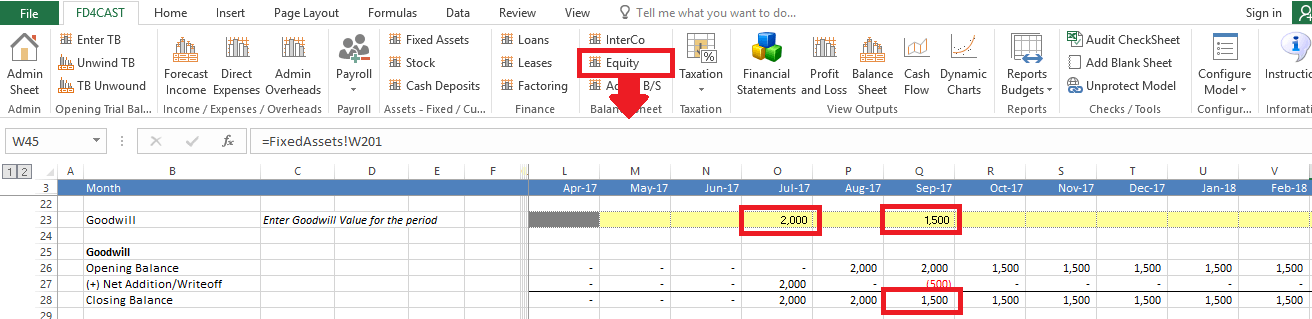

Revaluation of fixed assets and goodwill are reflected in Equity section under Revaluation Reserves. Any subsequent adjustments to the initial revaluations are also reflected here.

Initial recognition of goodwill as well as subsequent revalued amount is entered into the below section. Keep in mind that in case of revaluating initial goodwill, user must enter the ending value for the period rather than the amount of adjustment.

In the example above, goodwill is initially recognized in the month of July. In September it is revalued downward to £1,500. We enter revalued amount in yellow cell in the corresponding period.

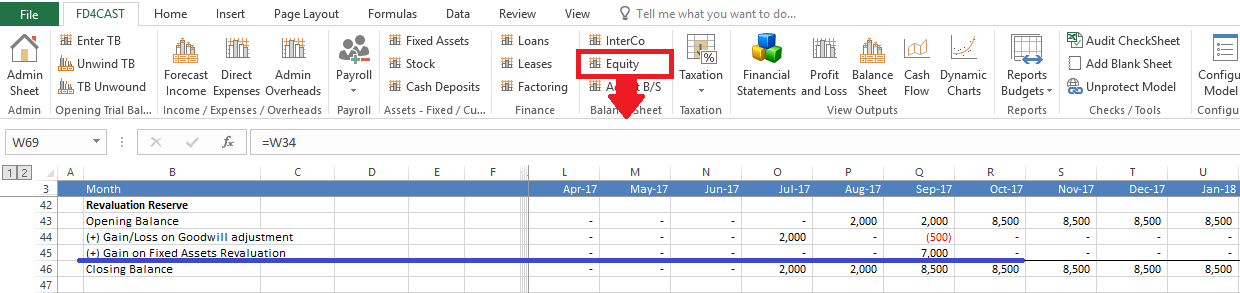

Fixed Asset revaluations are also reported under Revaluation Reserve section on the Balance Sheet. For detailed instructions on how to revalue fixed assets, please, review Section 4.1.2: Fixed Asset Revaluations.

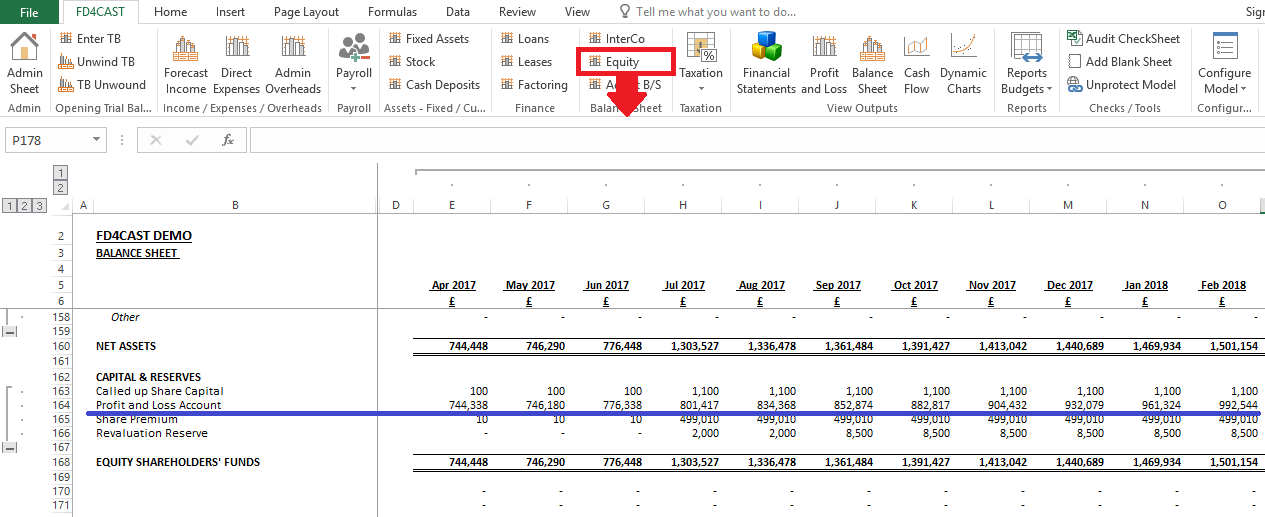

Accumulated profits/losses are reported under Profit and Loss Account in Equity Section. This is the same as retained earnings account.