Financial Statements of the company can be accessed from the View Outputs group on the ribbon. All throughout the previous sections we have reviewed how specific items, like income & expenses, fixed assets, loans, leases, etc. impact all three financial statements. In this section we will discuss their structure and content.

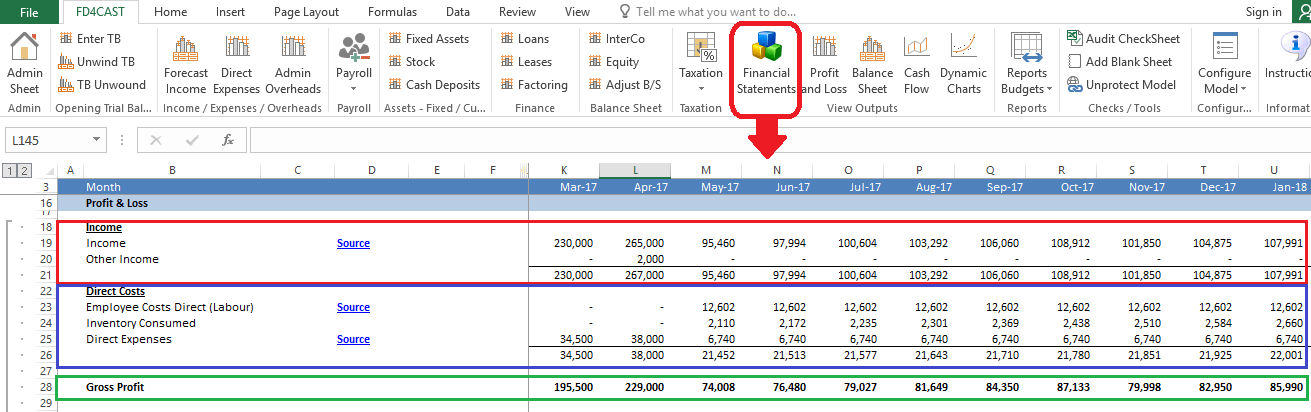

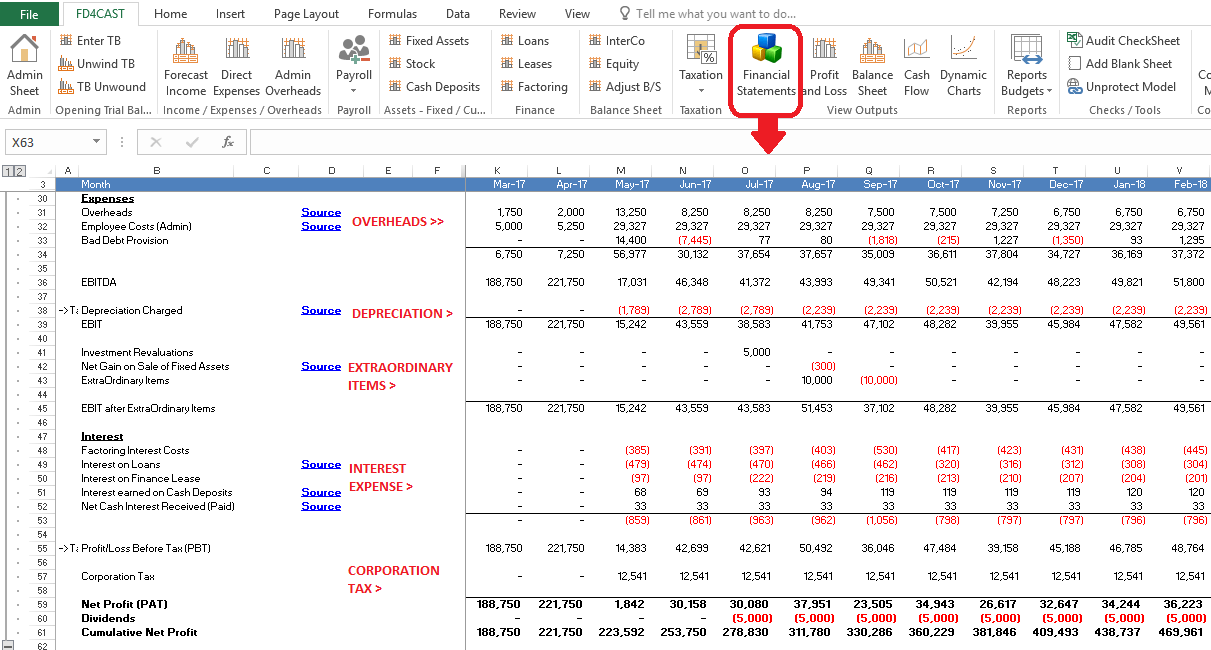

At the very top of Financial Statements Section, we have a Statement of Profit & Loss which can be reviewed by expanding the corresponding group rows. P&L consists of several account groups: By subtracting Direct Costs from Income, we arrive at Gross Profit.

Cumulative Net Profit is calculated by subtracting Overheads, Depreciation, Extraordinary Items, Interest Expense, Corporation Tax and any Declared Dividends from Gross Profit. Each account and its calculation can be accessed by clicking on corresponding Source hyperlink.

Balance Sheet consists of Assets and Liabilities. Assets are divided into long term and current assets. Liabilities include long term and short term liabilities as well as the Equity. Total Assets and Total Liabilities balances must be equal for each period.

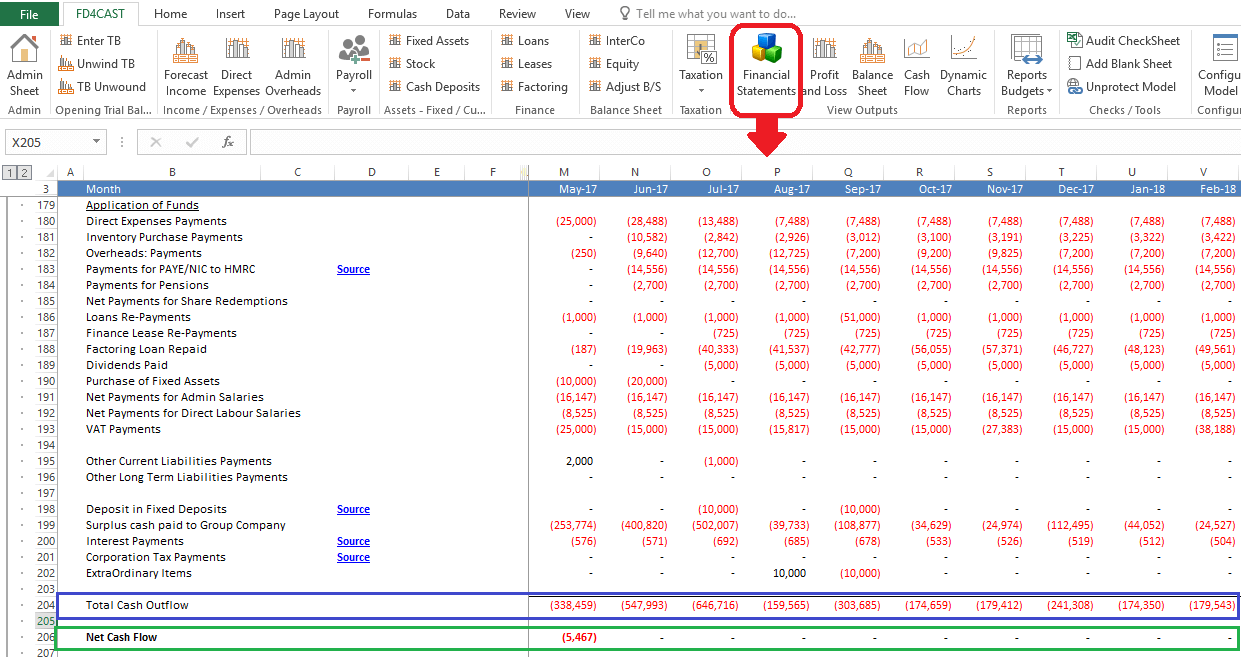

Both Direct and Indirect Cash Flows are included in Financial Statements Section.

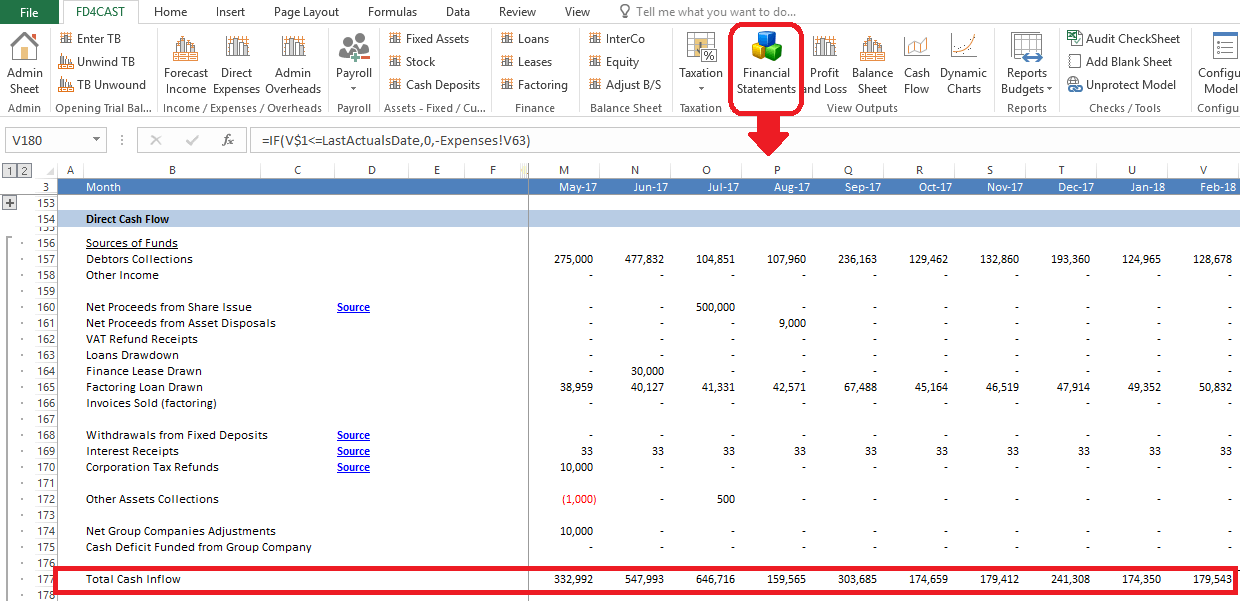

In Direct Cash Flow, total cash inflows are subtracted from total cash outflows to arrive at net cash flow for the period.

Total Cash Inflow:

Total Cash Outflow:

Indirect Cash Flow shows Profit/Loss Before Tax for the period. This amount is adjusted with non-cash items, non-operating expenses and working capital changes to arrive at Net Cash Flow from operating activities.

Cash flows from Investing and Financing activities are the same for Direct and Indirect Cash Flow formats.