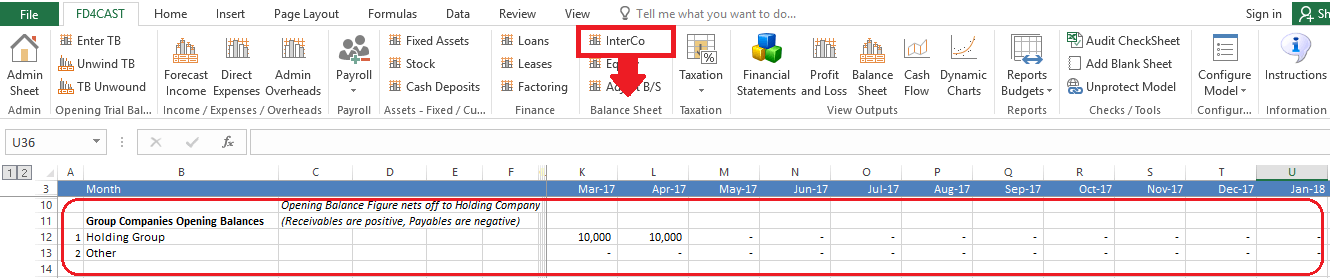

Model allows the user to easily manage InterCompany transactions from the InterCompany Section in the Balance Sheet Group on the ribbon.

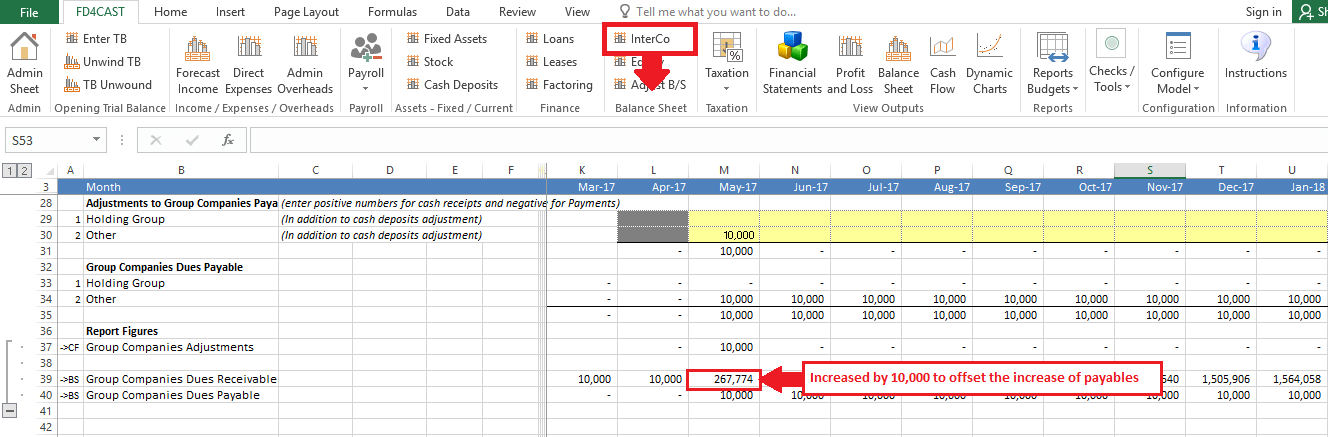

At the very top of the InterCompany section, opening balances of receivables/payables (+/-) with group companies are automatically imported from trial balance input.

In our example, the opening balance of £10,000 receivables is related to the holding company.

In order to add other group companies to the list, please review Section 1.4.2 Add/Remove Category Rows.

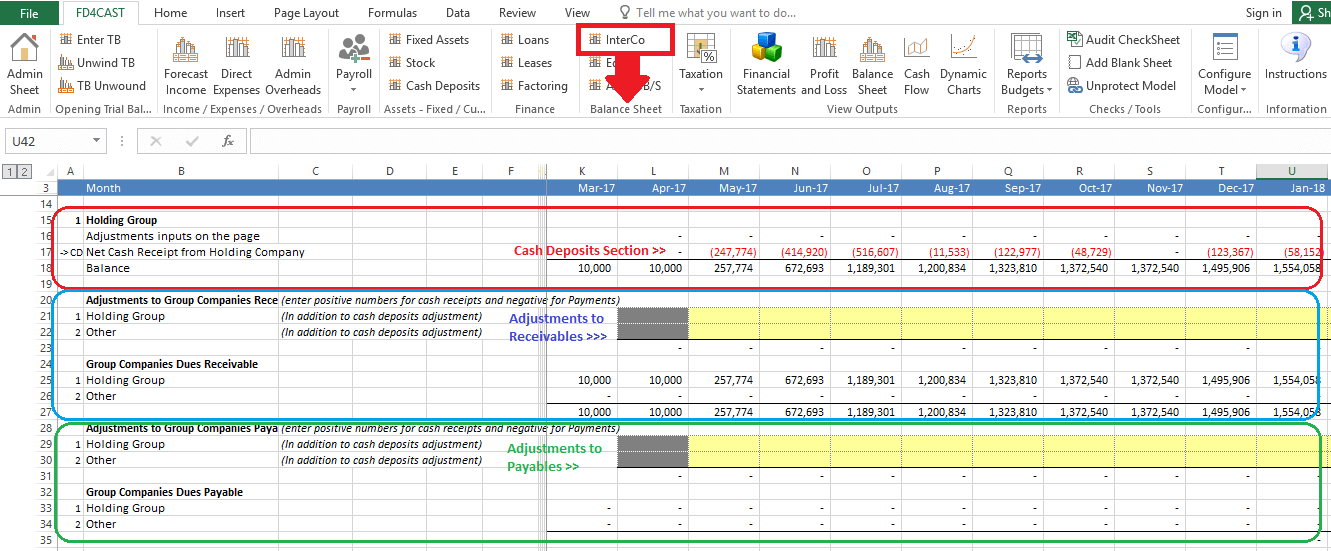

Net cash inflows/outflows to and from group companies are managed in Cash Deposits section. Final net figure for each month is imported into the current, Inter Company section. For more details on how to manage target net cash flow with the holding company, please, review Section 4.3.3 Transfers to / from holding company.

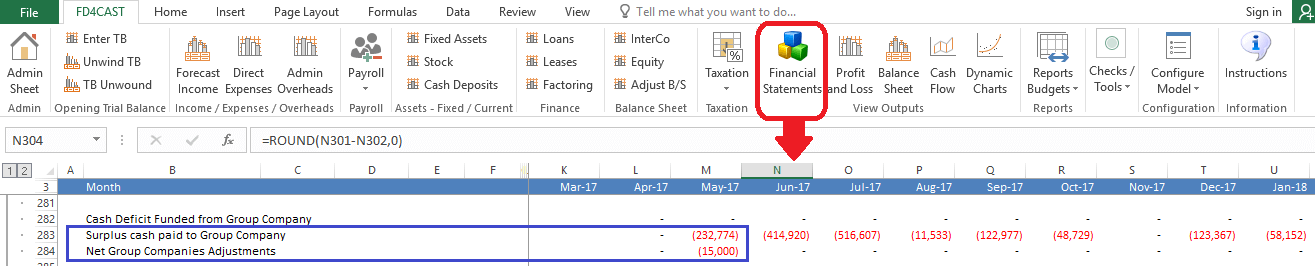

In our example above, target net cash flow with the holding company in the month of May is -£247,774. In combination with the beginning balance of £10,000, we get £257,774 of receivables balance with the group companies at the end of the period. This figure is fixed as it is our target balance with the group companies for the end of May-17.

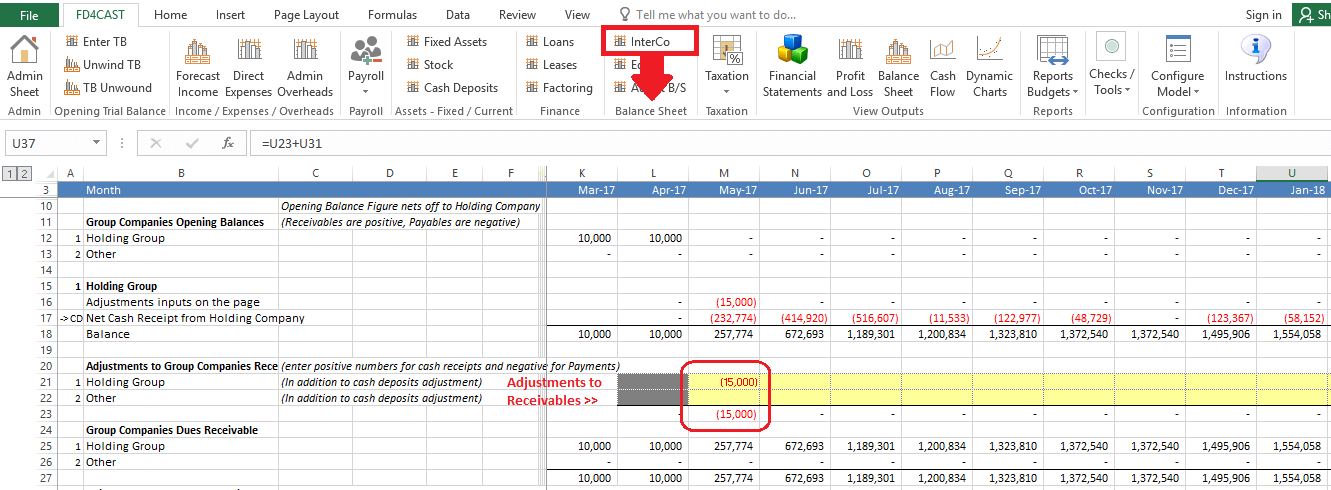

Yellow cells for receivables and payables enable the user to reflect any adjustments to the net cash flows with the holding company. This feature can be used for financial statement consolidation purposes. E.g. if £15,000 out of £247,774 transferred to the holding company was in transit by the end of May-17, we will enter -£15,000 as an adjustment to receivables.

As a result, net cash outflow to the holding company will be reported under two separate headings on the Statement of Cash Flows: Surplus cash paid to Group Company (this amount will be used for consolidation purposes) & Net Group Companies Adjustments that will be reported as cash outflow from financing activities for the period.

In another example, if the company received £10,000 from the group company we can enter this amount in Adjustments to Payables. Increase in payables to group companies is automatically offset by increase in receivables. This way our target net cash flow with the group companies remains unchanged.

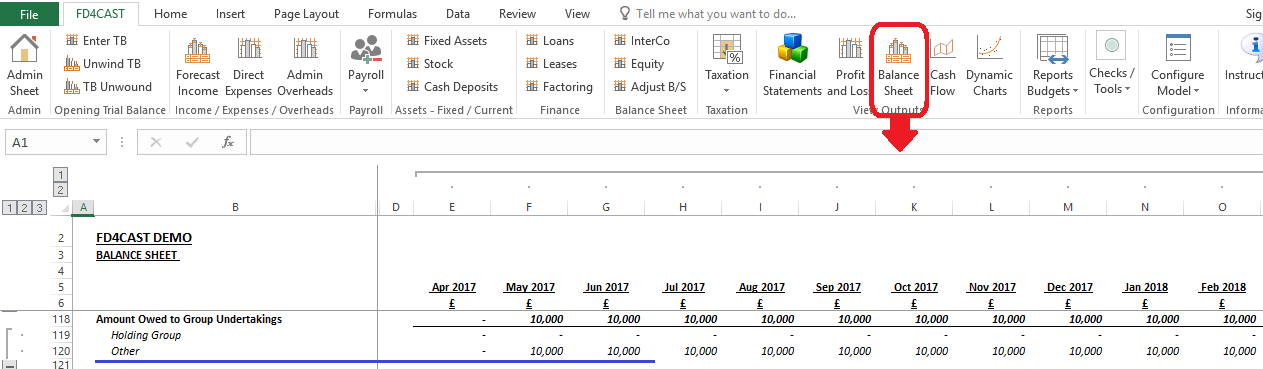

Increase in payables will be reflected on the Balance Sheet under ‘Amount owed to Group Undertakings’: